Methods to the Messari Madness - Unqualified Opinions

a call for comments on our open token supply methodologies

Your daily snapshot from the OnChainFX markets dashboard.

We caught a lot of heat for our late January report on Ripple, and how the XRP market cap was overstated by some $6 billion at the time.

Most of the flak came from the #XRPArmy, but some stemmed from legitimately interested critics. The latter argued Messari was applying an inconsistent standard to a single asset; we were picking on Ripple, and not using similar rigor on our other supply estimates.

Of course, that’s not entirely true.

Before we published our report, we had worked for months on our own supply methodology. One that serves as the backbone of the Messari registry participants’ supply curves, and that we hope will soon replace the de facto standard “circulating supply”, a measure that is often inaccurate to an extreme.

Ripple was simply the most obvious and material culprit of “market cap inflation.” Others are less obvious.

Supply characteristics of cryptoassets differ from all other asset classes. Issuance of new supply is determined by a mix of algorithmic issuance, asset creators’ discretion, decentralized stakeholder voting, etc. The variety of approaches taken across the top 20 assets, not to mention the thousands of other existing assets, is extreme.

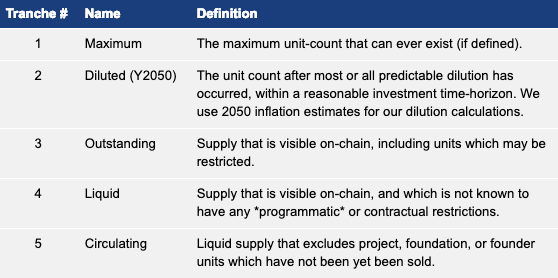

These assets require novel, but precise ways of defining and discussing supply. It’s time to retire terms like “circulating supply”, “available supply”, or simply “supply” unless they are properly defined. Instead, we propose more precise definitions for several different cryptoasset supply tranches.

Our goal is to create a sensible reference data standard that can be used across the entire industry, while also mapping our definitions to existing alternatives like that of CoinMarketCap.

We propose that most assets have the following categories of supply: maximum (defined cap?), diluted (read: our Y2050 estimates), outstanding (on-chain), liquid (unrestricted), and circulating (held outside of known founder wallets). With those inputs we can more accurately discuss the “market cap” of a given asset.

We also recognize that analysts need to estimate things like annual inflation and token loss estimates.

We introduced the concept of Y+N to OnChainFx this past weekend with our addition of “Y+10” estimates. In the coming months, we’ll also allow filters for Y+1, Y+3, and Y+5, and eventually allow users to pull a truly custom Y+N estimate for any given asset (and any given model).

Finally, we are working on an “Active-X” supply function, which allows anyone to build activity graphs to parse wallet addresses by their activity or dormancy over a defined period of time.

These are important definitions, and we hope you’ll join this important conversation.

Let us know what you think of Messari’s Method for token supply curves. We’ll be opening up a number of our other data methodologies in the weeks ahead.

Read the full methodology here.

The more rigorous and ubiquitous our investor terminology, the faster the asset class will scale. We’re happy to play our (small) part in that growth.

-TBI

P.S. Spread the love. Tweet at Messari for requests, feedback, comments, or questions.

Best of the Rest - What We Missed Last Week

Every weekend, we dig through the posts from crypto’s other great sources of content to see what we missed in our own weekend reads.

Here’s a few things worth reading to start the week:

The Virtuous Circle of Market Data - Noelle Acheson

Flows in crypto data resemble the intent behind early stock market information distribution to a limited extent, explains Noelle. Data is useful for increasing liquidity and attracting new investors who in turn improve the flows of data with more information and better analytics which leads to higher levels of trust and comfort. This virtuous cycle of market data will be a crucial player in the maturation of the digital asset industry.

Blockchain Got Boring, Boring is Good - Patrick Tan

The term “blockchain” seems to have become pretty boring, especially compared to its use as almost a filler word a year ago, explains Patrick. But boring is good because the buzzwords start to subside, real use cases and hard-working teams shine, and this new technology begins to “move out of the pilot phase” into a moderately more mature industry.

Facebook Plans to Become World’s Biggest Central Bank? - Lance Ng

According to the New York Times, Facebook is creating its own cryptocurrency which will undoubtedly send tremors through the young digital asset industry. But the social media behemoth could also position itself to categorically disrupt financial banking if its rumored stablecoin project is a success, with billions of users connected to Facebook via Messenger, WhatsApp and Instagram.

Did I miss something?

Send me the link, your twitter handle and your best imitation compression algorithm write up. If I like it, I’ll include your bit next issue (with attribution).

Should your colleagues read daily? We now offer discounts for corporate access. Email us, and we’ll onboard your whole team.