We Love You (and Miss You) - Unqualified Opinions

We Love You (and Miss You) - Unqualified Opinions

swipe right on Messari's premium research. we're better than your ex.

You’ve been missing out on your daily dose of crypto, fam.

Below is a glimpse of some of the punchy research we’ve been sending out to our professional subscribers.

Don’t get us wrong, we still *love* our thousands of more casual matches. But if you’re ready to settle down, make a leap with us, and take things to the next level…

Today, Qiao broke down MakerDAO’s valuation, and back-of-the-napkin’d the fair price of one of the few crypto assets you can actually value with a DCF. Earlier this week, we took a look at the DeFi vs. Web 3.0 thesis, and yesterday we broke down actual Dapp usage, all while curating the deluge of daily news and crypto analysis.

We’ve got more great stuff coming next week, and some *big* new premium features rolling out in March, which will be offered to subscribers before anyone else (BAE?) We pack a helluva lot more than $1 of value into each issue, and you’ll see that for yourself once you try out UO’s premium research.

Subscribe before the end of this weekend, and we’ll even throw in some Messari swag for you (or your significant other).

:-*

-TBI

(Know someone else who needs the love today? Who lost 90% of his savings and his girlfriend in 2018, but still believes in the correspondent banking killer? Who still only swipes right for $ETC? Who can’t quite grok bitcoin’s thermodynamic security?)

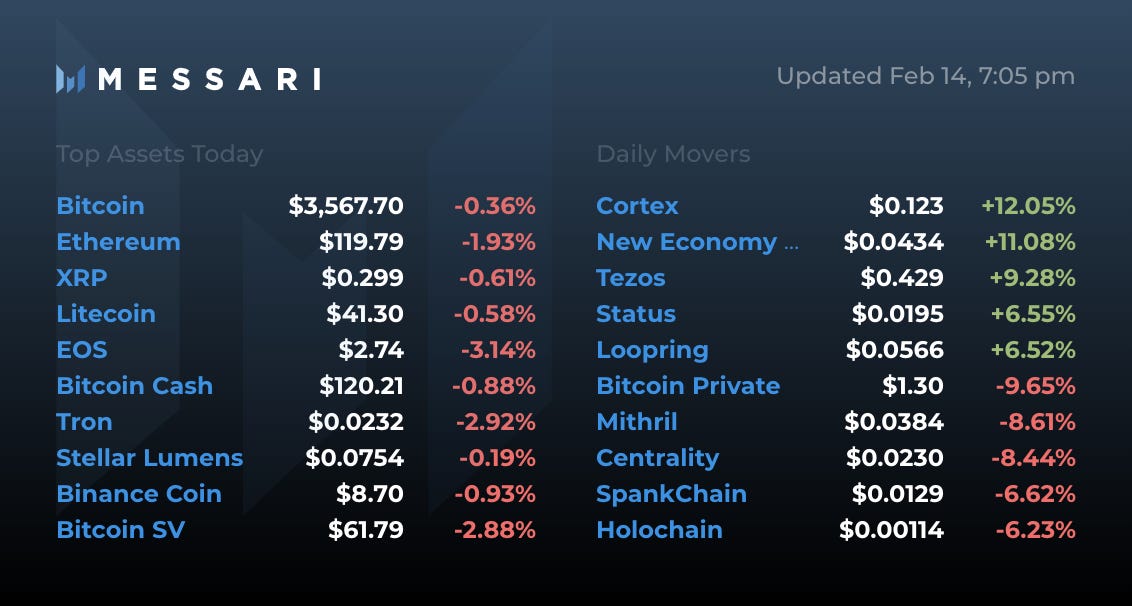

Your daily snapshot from the OnChainFX markets dashboard.

I was a big fan of Maker before it was cool. The idea is sound, and the team executes really well.

That said, as far as investing is concerned, the quality of the project is only half of the formula. The other half is how much you are paying for that quality.

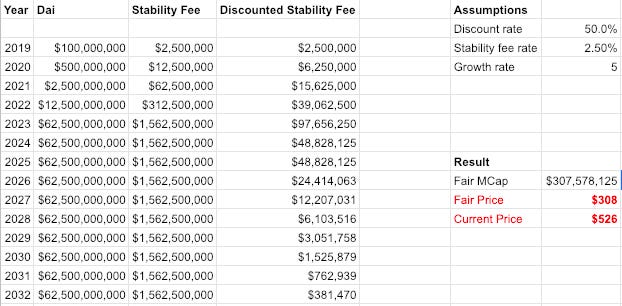

The nice thing about MakerDAO, as well as many other DAOs, is that DAO holders have rights to cash flow**. With Maker, the holders earn “stability fees” with each newly created collateralized debt position and Dai issuance. As such, you can make certain assumptions and use a discounted cash flow (“DCF”) model to get a sense for how much the token is “worth”, relative to the price you’d be paying.

This contrasts with, for instance, base layer tokens which are incredibly hard to value. As a former trader, I have strong opinions on valuation, and truth be told, almost none of the valuation frameworks on base layer tokens I’ve seen so far makes any sense.

[The only sensible valuation framework for base layer tokens is one that is based on the total addressable market of a global money. But I digress.]

I recently did some back of the napkin valuation work, and it looks like MakerDAO is fairly priced at best. Probably overpriced. But certainly no bargain.

What assumptions am I making here?

A very aggressive assumption of a 2.5% stability fee, which is the reward that’s paid to MakerDAO for governing the protocol. Currently the stability fee is 0.5%, but there are chats about raising it to 2.5%. A 5x increase would be a meaningful move from baseline assumptions, indeed.

A very aggressive assumption that the DAI supply will increase by 5x YoY over the 5 years and stabilize afterwards. This will put the DAI’s terminal supply at a whopping $65B. That’s over 30 times the supply of Tether. That’s also 5 times the current market cap of Ethereum, which means that in order for this assumption to become a reality, the market cap of Ethereum will have grow enormously in order for the network to be secure.

A VC-style discount rate of 50%.

Despite these aggressive assumptions, the fair price implied by the DCF model is way below the current market price. More than 40% lower, actually.

When I first posted this analysis on Twitter, one of the most interesting pieces of feedback I got was that, in 2018, DAI holders paid a lot of liquidation penalties to PETH holders, which were in fact way larger than the stability fees they paid to MakerDAO holders. When the multi-collateral version goes live, the liquidation penalty will go to MakerDAO holders. As such, MakerDAO holders will earn a larger cash flow in the near future.

But a fair counter to that is that the 2018 liquidations cascaded during a 90% down bear market. CDPs get liquidated when the value of Ether falls too quickly. But, if and when the aggressive assumptions we laid out above become realities, we will probably be in a massive bull market.

Just some food for thought.

-Qiao

** To be rigorous, MakerDAO uses a burning mechanism rather than cash flow mechanism. More precisely, instead of $1 worth of cash flow is distributed to DAO holders, $1 worth of DAO tokens are burned. The two mechanisms are almost mathematically identical, though.

TBI note: Qiao’s logic is going to be amazingly helpful if and when the market ever becomes rational and fundamentals driven. In the meantime, Maker has one of the strongest memes in crypto. Probably top three in terms of “narrative health” if there is such a thing, after only bitcoin and ether.

P.S. Spread the love. Tweet at Messari for requests, feedback, comments, or questions.

Messari Compression Algorithm

Content and thoughts from around the web as summarized by the Messari team.

🗳️ [Analysis] Humans: wonderfully complex, and often irrational - Meltem Demirors

Protocols are political. Governance sets the rules of the game and, like any other political game, the system changes as power disputes arise. The five largest networks with on-chain governance systems--EOS ($EOS), Dash ($DASH), NEO ($NEO), Tezos ($XTZ), and Decred ($DCR)--have various mechanisms to assign power. In other words, distribution of power and money differ by system. As these systems grow, they are bound to evolve based on power disputes. As voting patterns are highly correlated to incentives, expect these networks to resemble oligopolies at best, cartels at worst. (share or read more)

🏛 [Analysis] A thread on SEC Commissioner Hester Pierce's crypto regulatory speech - Patrick Berarducci

Hester Pierce's recent speech on SEC regulation practices concerning crypto assets is raising eyebrows. Crypto assets are often called investment contracts and therefore securities. Yet, a crypto asset is really only usable software, both legally and practically. If the SEC claims crypto assets are securities, they will more than likely lose in court as the argument is too vague. The years lost battling such action, however, would be extremely detrimental to the industry. The SEC's concern for protecting investors is warranted, but the industry is arguably doing a better job self-regulating, anyway. Disclosures and transparency projects are growing more common. (share or read more)

Quick Bits (Don't read that, I read it for you)

Choke Points (Exchange News)

👉 Nasdaq is adding the Bitcoin ($BTC) Liquid Fund and Ethereum ($ETH) Liquid Fund to its list of 40,000 indexes. The two indexes are provided by Brave New Coin and list the most liquid prices available on the market. The indexes will be added by the end of the month. (share or read more)

Startup Signals (ICOs, Cryptos, and Startups)

📣 SKALE Labs Inc. launched its testnet for its mainnet launch planned for Q3 2019. SKALE allows Ethereum ($ETH) developers the ability to launch application specific sidechains. SKALE is expected to have magnitudes of order larger throughput than Ethereum Layer 1. (share or read more)

😳 J.P. Morgan has announced that it will offer an internal stablecoin called JPM Coin for select customers. JPM Coin will be used for transfers between institutional accounts and is backed by U.S. dollars. According to the company over time new currencies will be added to the platform, which is built on JP Morgan’s Quorum blockchain. (share or read more)

The Powers That Be (Legal/Reg/Policy)

⛔ The Securities and Exchange Commission (SEC) have asked for the withdrawal of a Bitcoin ($BTC) futures and sovereign debt backed ETF provided by Reality Shares ETF Trust. (share or read more)

Did I miss something?

Send me the link, your twitter handle and your best imitation compression algorithm write up. If I like it, I’ll include your bit next issue (with attribution).